EU and UK sugar market situation and outlook

19 January 2022

Julian looks back at how key drivers have impacted European sugar prices in 2021 and what 2022 may hold for market participants

Contents

- Weather update

- Macro-economic commentary

- EU and UK sugar market prices

- European sugar production estimates

- Sugar trade estimates

Weather and aphids

The weather across the European "sugar beet belt" this winter has been quite mild. Warm conditions persisted in the west and south, however, the north and east of the continent was cold. Overall, Europe has had its coldest December since 2012, although several countries experienced record-breaking warmth at the end of December. It was wetter than average across central and southern Europe, but drier-than-average conditions established in the Alps, Scandinavia, parts of Eastern Europe and of the Iberian Peninsula, Copernicus reports.

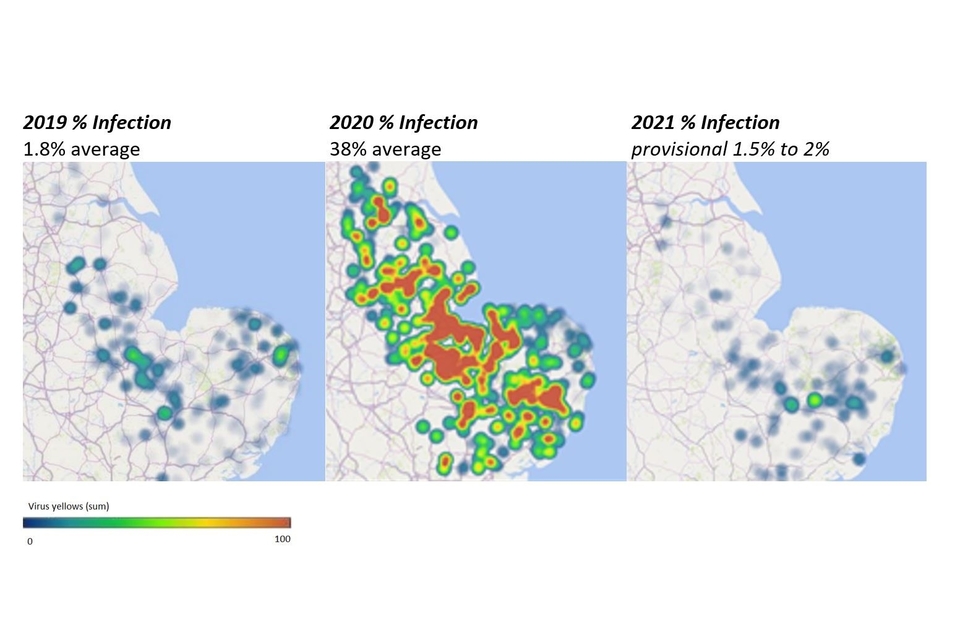

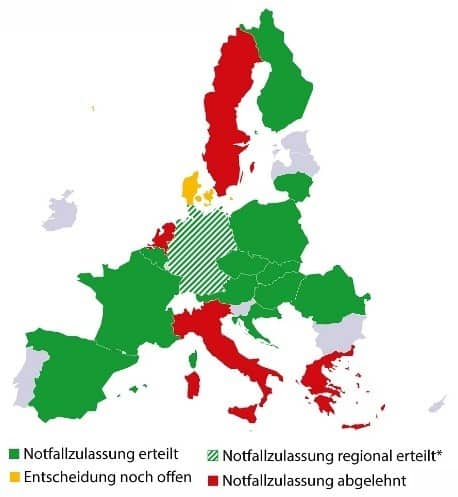

It is far too early to say if the mild weather may lead to infestation of sugar beet with aphids in 2022, there is of course still plenty of time for a cold snap to kill these vectors of virus yellows disease. But the authorities in the EU27 and the UK are not taking any chances! So-called "emergency" authorizations for neonicotinoid treatment of beet seeds are already available in 10 EU member states (see map below), which Brussels prohibited in 2018 to protect bees, and now the UK may join the list. On 14 January 2022, the UK government, "after careful consideration of all the issues", decided to grant an application for emergency authorisation to allow use of a product containing the neonicotinoid thiamethoxam, "in recognition of the potential danger posed to the 2022 crop from beet yellows virus". In 2021, the Health and Safety Executive had received an application from the National Farmers Union (NFU Sugar) and British Sugar seeking emergency authorisation for the use of the neonicotinoid product as a seed treatment on sugar beet. The product is Syngenta's ‘Cruiser SB’. There are, however, strict conditions to the UK emergency authorisation based on the beet yellows virus (YV) incidence prediction model developed and run by Rothamsted Research. This model will provide, on 1 March 2022, a forecast level of YV infection based on winter temperatures. In 2021 the YV threshold was set at 9%, and the predicted incidence was 8.37%, therefore the use of Cruiser SB was deemed not necessary. For 2022, the UK government has decided to increase the threshold to 19% of YV predicted by the model.

European Sugar Markets

"Macro" factors

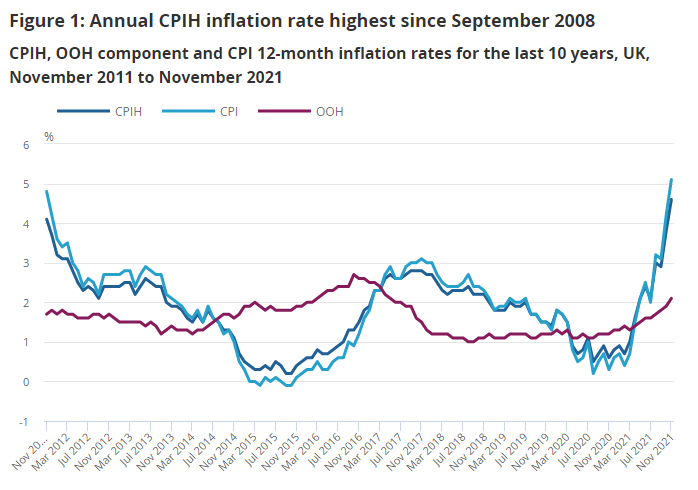

Early last year, inflation was just stalking the global and European economies. Today it has well and truly reared its ugly head, and nowhere more prominently than in the energy markets. The HICP measure of inflation is expected to reach above 5% in the euro area overall, and up to 12% in the Baltic States. In the UK, the CPI measure of inflation rose by 5.1% in the 12 months to November 2021, up from 4.2% in October. In the US, inflation has now reached 7%, it's highest level in 40 years.

.png)

And energy markets are continuing to trade higher in Europe, as "as hyperinflation in natural gas and power prices hits homes and factories across the continent", according to Citigroup. Gas and electricity, rather than oil, are the main drivers. Using current forward prices, the region’s total primary energy bill will come in at about $1 trillion (before adding on CO2 costs), the bank said in a report. That compares with about $300 billion last year and $500 billion in 2019. Carbon prices are also soaring, with prices for EUAs (European Union Allowance – the official name for the region’s emission allowances) reaching above USD 80 per tonne, up from about USD 30 a year ago. Not surprising, then, to see ethanol T2 (Platts) futures trading around EUR 1,000 per metre cubed, up from around EUR 500 a year ago. Nevertheless, ethanol for motor fuel remains about half the price/litre of petrol in France (0.87 USD/l vs 1.93 USD/l, both TTC), according to https://www.globalpetrolprices.com/.

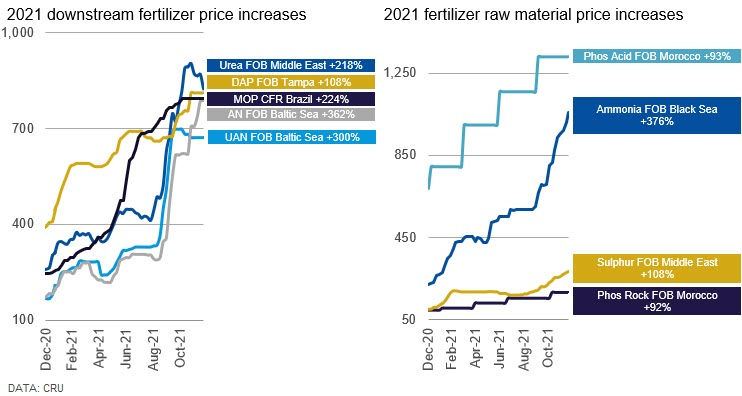

And fertilizer prices at least doubled in 2021, although in January 2022, urea and other fertlizer component prices fell back a little. Meanwhile, the Baltic Exchange's dry bulk sea freight index has dropped to its lowest level since April 2021 on Tuesday, weighed down by weaker demand across all vessel segments, Reuters reports. In the container markets, however, the ‘Mother of All’ supply shocks lurks in China’s Covid crackdowns, Bloomberg reports, quoting a warning from HSBC economists who caution that if the highly infectious omicron variant which is already swamping much of the global economy spreads across Asia, especially China, then disruption to manufacturing will be inevitable. According to UNCTAD’s Review of Maritime Transport 2021, if the current surge in container freight rates is sustained, this could increase global import price levels by 11% and consumer price levels by 1.5% between now and 2023.

European sugar and sweetener prices

As usual, European sugar markets have been rather slow to respond to these "macro" factors. In France, CGB reported on 11 January 2022 that spot sugar prices are around EUR 550 per tonne ex-mill. However, as noted in Sugaronline's EU cash prices series, European and UK sugar prices have declined by around EUR 40 from the highs seen just before the 2021/22 sugar beet campaign began to get underway, tracking down the decline in import parity prices as the world market denominated in EUR began similarly to fall.

At the 16 December 2021 meeting of the CMO Arable Crops Committee, the European Commission reported that the average EU27 invoiced price for sugar rose to EUR 417 per tonne ex-mill in October 2021 with a standard deviation of 27 EUR/tonne. The outlook for November based on Eurostat data is for the average price to rise by EUR 10 to around EUR 427 per tonne and thereafter, based on Sugaronline's assessments, to have declined a little in January 2022. Unlike the prices reported under short-term contracts, the average reported prices may have been negotiated between buyer and sellers months or even years before delivery. In the "deficit area" Region 3, the average invoiced price was reported to be EUR 479 per tonne ex-mill, reflecting a widening difference in prices between region 3 and regions 1 and 2. The meeting also noted that average prices under short-term contracts were around EUR 28 per tonne higher than the average invoiced prices. Meanwhile, so-called "spot prices" (newly negotiated sales) continued to rise in recent months, according to the Commission. In the countries around the Mediterranean Sea, spot prices were seen around EUR 635 per tonne [presumably delivered], while in the main production countries in the EU (region 2), spot prices were seen around EUR 590 per tonne.

The European (EU27) market for white sugar (sucrose) amounts to around three-quarters of the total nutritive sweeteners market (it might be assumed from intra-EU trade data). Glucose and isoglucose dominate the remainder. Typically, prices for glucose tend to remain quite static whilst those for isoglucose trade at around 55% to 60% of the price of sucrose. Recently, however, isoglucose prices have risen quite markedly, according to Eurostat Intra-EU trade data, reaching 70% of the (rising) equivalent price for sucrose. In November (the latest data available), Eurostat recorded that the average price of isoglucose in intra-EU trade was EUR 338 per tonne compared with the equivalent for sucrose of EUR 485 per tonne.

European sugar production estimates

EU27+UK sugar production is expected to reach around 17.2 million tonnes from the 2021/22 campaign, which in many countries is now ending, a little below the levels seen in 2018/19 and 2019/20. Sugar production in France is expected to reach just above 4.4 million tonnes (excluding DOMs), some 90% of the average since 2017/18. Production in Germany is also expected to reach around 4.4 million tonnes, pretty similar to the average since 2017/18. Sugar production in Poland has reached the highest level for three years, and Austrian and Slovakian sugar production is expected to be higher than in recent years. However, production in Belgium, Croatia, Hungary and Spain is expected to be lower this year. Sugar production in the UK is expected to be slightly disappointing at around 1.05 million tonnes.

Turning to the 2022/23 campaign, the area sown to beet in the EU27 this spring is expected to be roughly the same as it was in 2021/22, which would imply that the EU-27 will remain in deficit, reliant on imports to fulfil demand. However, the stronger gross margins available to farmers from higher maize, wheat and OSR may have limited sowings of spring sown sugar beet, meaning that the EU market may fall deeper into deficit - only time will tell!

In the UK, things are looking more encouraging for the 2022 spring sowings, the NFU and British Sugar having agreed to increase sugar beet prices by a headline-grabbing GBP 5 per tonne to GBP 27 per adjusted tonne under one year fixed price contracts, but there will be no market linked bonus. For 3-year agreements, the price is fixed at GBP 25 per adjusted tonne, an increase of GBP 3.82 per tonne. For up to 10% of the quantity, sugar beet farmers may opt to price beet against a futures-linked variable price contract, an option which is now extended to all farmers. It is notable that sugar farmers in the EU27 - notably France - are angling for similar futures-linked sugar beet pricing formulae. The new UK contract also includes a Virus Yellow crop assurance scheme, although the insurance scheme may not be required thanks to the UK ministry DEFRA having approved an emergency temporary authorisation for the use of neonicotinoids for the 2022 sugar beet crop in England (see above).

Imports and exports

Imports of all types of sugar into the EU27+UK in the new marketing year ending September 2022 reached 431,000 tonnes in November 2021 (including IPR), Eurostat and ONS data published on 14 January 2022 showed, of which 105,000 tonnes was imported into the UK. The quantity recorded is relatively high compared with imports recorded by the same time in previous marketing years. However, as in 2020/21, imports from ACP countries, LDCs and South Africa were markedly lower at 169,000 tonnes by November 2021.

It is clear from the Eurostat and ONS data that ACP, LDC and South African exports to the EU27 and the UK have been substituted ton-for-ton by imports under the UK Autonomous Tariff Quota (ATQ) of 260,000 tonnes per annum. On 21 December 2021 the UK Government announced an extension of the 260,000 mt Autonomous Tariff rate Quota (ATQ) for raw sugar for refining for three additional years until 31st December 2024, following what it called an "evidence-based" review. The announcement was greeted with condemnation from CEFS, NFU Sugar, who said that UK beet growers would be devastated by the ATQ extension, and the ACP/LDC Sugar Industries Group, who asked, "how [can] the UK Government’s trade policy be reconciled with the Government’s commitment to reducing poverty through trade?", whilst stating that it is vital to have a viable cane refining sector in the UK. Compounding the bad news for ACP and LDC sugar suppliers, hot on the heels of a trade deal with Australia, signed on 16 December 2021, which will provide for a sugar quota of 80,000 tonnes of Australian sugar to the UK, rising by 20,000 tonnes per annum until full liberalization after eight years, on 13 January 2022, the UK announced that the UK and India has launched negotiations on an ambitious Free Trade Agreement; it is not known if sugar would be part of that, but very probably.

Applications for import licences into the EU27 appear to slowed down so far in January, according to data published by the European Commission. So far, the total of licence applications granted to operators has reached 13,000 tonnes, the majority for imports from Serbia.

As might be expected EU27 exports of sugar to third countries have got off to a slow start, with 186,000 tonnes exported in 2021/22 up to November, according to the latest Eurostat data. The vast majority of these exports are to nearby countries such as Switzerland and Norway.

Meanwhile, within the EU27+UK market, intra-EU trade has slowed down a little, perhaps implying that sugar producers concentrate on local markets rather than exports ... certainly that's the case with exports to third countries. The Power BI visual available by clicking below allows one to scroll through the quarters to see how the intra-EU sugar market has evolved over time.

Click here and then select "Intra-EU trade flows"End note: I hope that you will explore the interactive charts in this report. With a few clicks of your mouse, you can drill down into the data and gain - I hope - a deeper appreciation of the EU and UK sugar market situation. All comments and suggestions most gratefully received!